A strengthening housing market forecast is pointing toward a significant recovery in 2026, with NAR economists expecting home sales to climb as mortgage rates ease, buyer demand improves and price growth continues despite mixed market conditions.

HOUSTON — Real estate professionals may finally see a long-awaited surge in activity in 2026, with home sales poised for a potential double-digit jump.

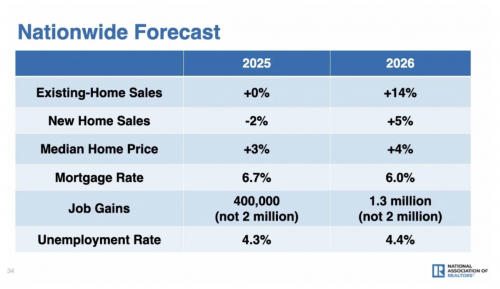

Lawrence Yun, chief economist at the National Association of Realtors®, is forecasting a 14% nationwide increase in home sales for 2026, following 2025’s stagnating levels. New-home sales are also projected to rise 5% next year.

“Next year is really the year that we will see a measurable increase in sales,” Yun told attendees Friday at the Residential Economic Issues and Trends Forum during NAR NXT, The Realtor® Experience, in Houston.

Rising sales won’t come at the expense of stability either: “Home prices nationwide are in no danger of declining,” he said. NAR expects prices to climb 4% in 2026, supported by job growth and persistent supply shortages.

Early momentum: Jobs, mortgage applications and builder activity

The groundwork for a rebound may already be forming. Mortgage applications are trending higher, job gains remain steady, homebuilders continue to add supply, and the record-breaking 43-day government shutdown — which could have delayed some transactions — has finally ended, Yun said.

“Mortgage applications have been consistently above last year, implying that people’s desire to enter the market has been consistently positive,” Yun explained. In the latest week, mortgage applications for home purchases surged 31% higher year-over-year, the Mortgage Bankers Association reported.

Mortgage rates: A slow drift downward

Mortgage rates remain one of the biggest constraints for buyers. After sitting around 7% earlier this year, the 30-year fixed rate averaged 6.24% this week, according to Freddie Mac.

Yun expects gradual improvement ahead. “As we go into next year, the mortgage rate will be a little bit better,” he said. “It’s not going to be a big decline, but it will be a modest decline that will improve affordability.”

He forecasts rates to average around 6% in 2026, down from a roughly 6.7% average for this year.

While the Federal Reserve has initiated rate cuts, Yun cautioned that mortgage rates are influenced by many variables — including inflation, Treasury yields and federal borrowing. Buyers should not expect a return to 3% rates anytime soon. Still, even modest declines could unlock significant buyer demand, he added.

A market of haves and have-nots

But the path to a 2026 rebound will not look the same across the market, which remains highly uneven.

“The upper end of the market has been doing much better than the lower end,” Yun said, noting strong inventory and financial markets driving activity. Sales in the $750,000 to $1 million range have shown some of the strongest gains, while lower-priced inventory remains tight.

NAR Deputy Chief Economist Jessica Lautz also highlighted the widening divide between buyers with home equity and first-time buyers.

“We have haves and have-nots,” she explained. “First-time home buyers are really struggling to get in, while those who have housing equity are building credit.”

According to NAR’s newly released 2025 Profile of Home Buyers and Sellers, first-time buyers dropped to an all-time low of 21%, far below their historical 40% share. They are also older than ever, now with a median age of 40.

Young adults continue to aspire to homeownership, Lautz noted, but obstacles like high rents, student loans and childcare costs remain significant. Better education about down payment assistance and special mortgage programs could help more buyers enter the market, she added.

Meanwhile, repeat buyers — especially baby boomers — are dominating transactions, often paying with cash or leveraging substantial equity.

Price reductions return as days on market rise

With seasonal slowdowns setting in, sellers are being reminded of the importance of correct pricing.

“It requires some price reduction in order to move the home,” Yun said. “Homes that sit on the market for long … will need to reduce the price to attract buyers.”

MLS data shows price cuts rising as listings linger. Yun shared average reductions based on days on market:

0–14 days: 4.9% cut

15–30 days: 6.1% cut

31–60 days: 7.3% cut

61–90 days: 9% cut

91–120 days: 10.6% cut

Over 120 days: 13.8% cut

Temporary dips may occur in local markets with rapid inventory growth, but Yun views these as short-term imbalances. Nationally, he expects a median 4% home-price gain in 2026 after a projected 3% gain in 2025.

Job growth, inventory trends and the 2026 outlook

Despite speculation about foreclosures increasing, Yun said market fundamentals remain sound, with mortgage delinquencies near historic lows, homeowners holding substantial equity and job growth remaining strong.

So, while 2025 has been mostly stagnant for housing, Yun believes the conditions are coming together for a meaningful recovery in 2026.